This is a continuation of a previous set of posts and is sixth in a series.

The most common question a VC gets asked is “What sort of deals do you invest in?” Most of them will give variations of the same answer… looking for a fast-growing market, strong technology, great management, at a fair price. And it’s nice to have milestones to know when you’re winning.

One at a time:

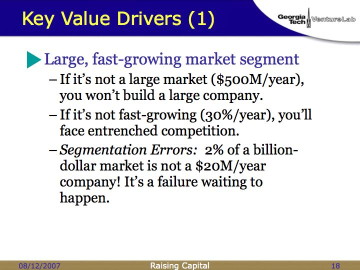

“Large” and “fast-growing” are both necessary and neither alone is sufficient.

If’ it’s not a large market, you can’t build a large company. Duh. You might utterly dominate the market for left-handed widgets, but if very few people want to buy left-handed widgets, you’re still going to be a niche player.

Less obvious is why the market has to be fast-growing. Classic example: automobiles are a multi-billion dollar industry, but (in the U.S.) sales are flat or growing at single-digit percentages. So becoming a new entrant there is suicidal, since the established vendors will fight to maintain their existing market position. And it’s very romantic to think of yourself as David versus Goliath… but Goliath usually wins.

(And dinosaurs lasted one heck of a lot longer than mammals have so far, and it took an asteroid to finally do them in.)

This is often linked to a segmentation error. Too many startups say something like “It’s a billion-dollar market; all we need is two percent, and we’ll be doing $20 million a year!”

Mistake. Mature markets shake out into patterns; a common one is a 50% player, a 30% player, a 15% player, and a bunch of losers. If you’re targeting 2% market share, you’re telling potential investors “I want to be a loser!”

So re-segment your market, and see if there’s a way to be a winner. Look at automotive again. Note that a new entrant like Tesla Motors isn’t saying that they’re going to be a 0.1% player in the overall vehicle market. They’re saying they’re going to be the dominant player in the market for electric vehicles. That shifts the question back to basics—is that segment big enough and fast-growing enough? That’s a much more useful discussion than arguing over whether you can capture 0.12% or 0.15% of a bigger, but mostly inaccessible, market.

(In 1992, John Sculley did this precisely wrong. He released the Apple Newton… but instead of claiming it would be the dominant player in a then-nonexistent PDA market, he kept talking about a $3.5 trillion converged market for computing, communication, and entertainment. His math was accurate, but suicidal. Newton sales of several tens of millions of dollars were actually pretty impressive… but as a percentage of $3.5 trillion, it looked like a complete failure. Oops. The Newton went away and, shortly thereafter, so did John Sculley.)

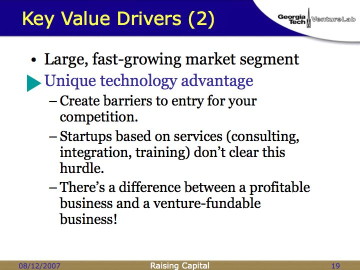

The next hurdle to jump is having a unique technology advantage. (Note that I do not say patents. Patents are wonderful, and nice if you can afford them, but there are other ways to build and protect a technology advantage.)

You’re really trying to create a barrier to entry for your competition. I don’t care how smart you and your engineers are… most of the smart people in your industry do not work for your company. And they’re not static—they’re going to try to figure out smart ways to compete with your new company. Deal with it.

John Warner of SwampFox points out that there are ways to build companies whose advantage is in supply chain, or other elements of value creation, not just technology. He’s right. But some of those start looking like service companies, and it’s hard for service companies to attract venture financing.

Why? Linearity. Most service companies—consulting, systems integration, training, etc.—have outputs that scale linearly with inputs. If you want twice as many lines of code, you need to hire twice as many programmers. If you want to teach twice as many courses, you need twice as many trainers. (Or a disruptive technology, which proves my point.) Linear scaling is fine, and you can make an excellent living that way… but you shouldn’t take venture money.

Go back to the Venture Equity Cycle chart. VCs need non-linear deals where you can double the inputs and see outputs increase 10x. Or 20x. Or 100x.

There’s a difference between a profitable, successful, attractive business and a venture-fundable business. Know which one you are.

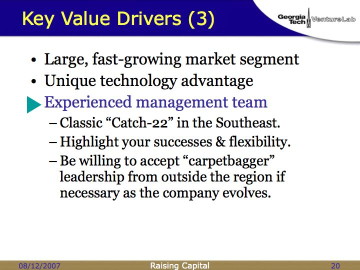

You need experience to get funded, but you need funding to get the experience. Catch-22. (Younger audiences tend to look puzzled at this point. Does no one read anymore? Sigh.)

The best possible CEO for your company is someone who has done something exactly like this twice already and has made money for the investors both times. If that’s not you, your investors will sooner or later start looking for that person. Cooperate.

There’s a whole discussion to be had on the lifecycle of CEOs (check out this book for a good overview), but the truth of the matter is, experience counts. You may not have the relevant experience. Worse, no one in your city or state may have the relevant experience. In the South, we call this the “carpetbagger” problem. Be prepared.

People who haven’t been through the process tend to think I’m lying about this one. But it’s true.

Yes, there are “vulture capitalists” out there, but if you do your homework, you can avoid them. Most early-stage venture investors really do want to see you get amazingly, ridiculously, gloriously rich. Because if you build a company with enough value that you get rich, the VCs get rich also. And so do their investors (see the Cycle again), and life is good for everyone.

And wealthy entrepreneurs are one of the best advertisements possible for a VC firm. (“Hey, team, XYZ Ventures backed Joe Doakes with his startup, and he just bought a personal dirigible! Let’s make sure we talk to XYZ before we show this deal to a bunch of other VCs.”)

We’ll talk more about terms later, but if you see any terms that make you start thinking of vultures… remember that vultures are carrion birds. They eat things that are already dead. If you company is alive and thriving, most VCs want to see you do well from it.

And if you have another path to raising the money—my “fourteen orthodontists” from the chart above—get some good advice as to what this might do to your capital structure, and what the consequences might be down the road. It’d be a shame if a poorly-structure

d $200K angel round now were to screw up your chances for a $4 million VC round later.

This one seems obvious, but a lot of people miss it. VCs aren’t going to hand you $4 million and say, “Great! Go build your widget and let us know when it’s ready. See you in a couple of years!” They’re going to want to see milestones. Initially, every month. Later, every quarter. And they’re going to want to know what’s Plan B (and Plan C, and…) if you miss those milestones. The most painful kind of lost venture money is money that’s pumped into a business after you should have already known it was in trouble.

(Side comment: treat milestones as truth checks. If you’re really not meeting them, maybe you should reconsider what you’re doing. Don’t scramble around hanging wallpaper and laying carpet to cover up fundamental cracks in your walls and foundation.)

The good news is, most VCs will not dictate those milestones; they’ll have input, but at the end of the day, you’ll be the one making the promises about what you can and can’t deliver. Make promises that you can keep.

So, if you look at successful startups, it’s like the opening of Anna Karenina: “All happy families are alike; each unhappy family is unhappy in its own way.” Experienced investors have seen enough deals, good and bad, to recognize patterns of success, and they’ll only invest in deals that fit those patterns.

If you’re outside of those patterns—you may be an excellent investment, but you are going to have problems finding a venture investor to step outside the box and take the risk.

(VCs are actually very risk-averse. Don’t let their public relations fool you.)