There has been a lot of noise lately about venture capital funds in trouble because their investors are missing capital calls. Which, at first blush, doesn’t make sense because venture funds are supposed to be “decoupled” from public markets. The key bit of knowledge that surprises many people is that venture funds don’t have any money. They’re not supposed to.

Venture funds don’t have Scrooge McDuck’s money bin (although it would be really cool if we did). They’ll typically have a business checking account with just enough money to cover a few month’s rent and utilities and travel expenses. The big money, the money that is invested in deals, comes from limited partnerships. The venture firm (I’m simplifying here) is the general partner, and large institutional investors or (very) wealthy individuals are the limited partners, or LPs. When “closing” a fund—which, confusingly, is what you call the initiating event; normal humans with shoe stores or law firms would call this the “opening”—the VC firm collects commitments for a certain amount of capital. But that doesn’t mean any money changes hands.

Instead, the VC firm issues “capital calls” to the LPs when it’s ready to make a deal. This will usually happen late in the diligence process, after the target company has accepted a term sheet.

Let’s make up XYZ Ventures, a hypothetical $100M VC firm (a bit on the smallish size nowadays, but it makes the arithmetic easier). Let’s further hypothesize that this firm got 15% of its committed capital from the state of East Virginia’s public pension fund… meaning East Virginia pledged $15 million over the “investment period” (usually five years).

Now our VCs, through luck and shoe leather, decide they want to invest $5M in SittingDuck.com. They’ll send out an email, followed by a phone call, to the East Virginia Public Pension Fund saying something like “We’ve identified a promising investment opportunity. We’re calling 5% of your capital commitment, which for EVPPF is $750,000. Please wire it to our transaction account within fourteen days.”

When things go smoothly, all the LPs wire their money the same day, and the money can be turned around and wired on to SittingDuck later that day, or the next day. At the worst, the venture fund sits on $5M overnight; the next day, the transaction account is back to zero.

Because venture funds are not in the business of holding cash… they’re in the business of holding equity investments. VC firms are far too specialized (and their expense ratio is far too costly) to manage cash. Every day that cash sits in their transaction account earning 2% is a day that it is not in a private company earning 25% or more. (Or zero, but that’s a different subject.)

Limited partners measure VC firms not only on their cash-on-cash multiple (“ten-baggers” and such) but on their rate of return, measured from the day of the capital call to the day of the ultimate distribution (after a sale, merger, or IPO). Sitting on cash earning 2% would inexorably drag down the eventual IRR for a particular deal, and eventually for the entire fund.

Which is a longwinded explanation of why VC firms don’t have any money, and why they practice “just-in-time” capital calls.

Now, firms are getting worried about their institutional investors defaulting on these calls. You can read samples here, here, here, and here.

But I haven’t seen anyone mention a critical element of this problem, which is asset allocation.

Most institutional investors (pension funds, endowments, family offices, etc.) will allocate their investments among a variety of asset classes: stocks, bonds, real estate, hedge funds, venture capital firms, and more. Venture capital (and hedge funds) are categorized as “alternative assets.” And most investors are going to allocate a relatively small percentage of their holdings to alternative assets. In many public pension funds, the maximum percentage is written into law.

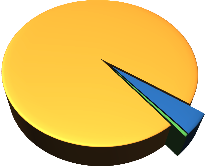

So, to keep the arithmetic easy, let’s say East Virginia’s public pension fund is a $10 billion fund. (East Virginia is a small state.) And let’s say that, since they are more enlightened than Georgia, they are allowed to invest up to 5% of that into alternative assets. They’ve been doing this for a while, so on August 31, 2008, they happened to have hit exactly 4.50% allocated, or $450 million. That allocation includes their $15 million commitment to our XYZ Ventures. Let’s keep making the arithmetic easy: they have 0.5% in cash, and 95% in a mix of stocks and bonds, including professionally-managed funds.

|

East Virginia’s asset allocation. Venture capital fits into the blue wedge. Cash is green. The yellow is “everything else”; it’s more complicated than I’m showing here! |

Then the bottom falls out of the market in the fourth quarter of 2008.

You’ve read the papers. The major part of EVPPF’s portfolio takes a huge hit. If they’re lucky, it’s 20%. If they’re not so lucky, it’s 40%. Let’s pick 30%.

What has happened to the value of the 5% in alternative assets? Venture capital funds (and hedge funds, but that’s beyond the scope of this already over-long post) are illiquid. You can’t look up their value on NASDAQ. So the valuations are whatever the fund managers put in their quarterly reports.

I’m writing this on the last day of January. Investors are just now getting their 4Q2008 reports. But, honestly, those valuations are going to look a lot like 3Q2008, and 2Q2008. Because VCs tend to adjust valuations of their portfolio companies only when there is some sort of transaction event. Initial valuations are at transaction cost—the price per share that the VC firm paid for them (less a discount for illiquidity). Obviously, a sale or IPO will trigger a re-valuation to the new price per share. Next best, a new venture round at a higher price with new independent investors will usually be sufficient for VCs to mark up their older shares to the new price (less a discount) in their quarterly reports.

In the other direction, if the company has raised money at a lower price (a “down round”), the VCs will have to adjust the valuation of their older shares downward… although various forms of anti-dilution can mitigate the impact.

But what if the company hasn’t raised money? Or if it has raised money, but not with a new independent investor to set the price? Normally, most VC firms will let the existing valuations ride, showing no gain or loss in the quarterly report.

Only in the case of a major problem with the deal—the CEO leaves, or a customer cancels a contract, or a product release slips substantially—will the VCs mark down their holdings in the absence of a transaction. And that doesn’t happen as quickly as it should sometimes. It’s not unheard of for a portfolio company’s valuation to be held at cost until it’s written down to zero when the company shuts down.

So the net result is that the valuations of the illiquid holdings

in a private equity firm’s portfolio don’t fluctuate very rapidly. Whereas the valuations of stocks fluctuate daily. Lately, most of those fluctuations have been down.

Back to East Virginia. On August 31, they had $450 million in alternative assets; let’s hypothesize that a combination of down rounds, shutdowns, and markdowns have eroded that valuation by 10% on December 31, 2008.

But we’ve already said that the rest of EVPPF’s portfolio took a 30% loss over the same period. Do the math:

| Asset Class | 31 Aug | % portfolio | 4Q08 ? | 31 Dec | %portfolio |

| Alternative assets | $450M | 4.5% | -10% | $405M | 5.7% |

| Cash | 50M | 0.5% | -0- | 50M | 0.7% |

| Stocks, bonds, etc. | $9500M | 95.0% | -30% | 6650M | 93.6% |

| Totals | $10000M | 100.0% | -28.9% | $7105M | 100.0% |

So what has happened here? EVPPF started off the fourth quarter with an asset allocation of 4.5% in alternative assets, comfortably within their statutory cap of 5%. We’re assuming they didn’t make any new investments during the quarter, nor did they receive any distributions. But the carnage in the public sector was so great that, without touching their alternative assets, they suddenly account for 5.7% of their shrunken overall portfolio.

And, even for money managers with MBAs, 5.7 is bigger than 5.

Ouch.

Depending on how strict East Virginia’s regulations are written, EVPPF may suddenly find itself in the position of having to dump fifty million bucks worth of perfectly sound alternative asset positions onto the secondary market (at a deep discount) just to get below their 5% limit.

At the same time, let’s say that XYZ Ventures has just found a great new deal and makes a capital call. EVPPF gets the call for another $750,000. EVPPF is still worth over 7 billion dollars, so this call represents 0.01% of their assets under management; peanuts, right? Our hypothetical conservative East Virginia managers are sitting on plenty of cash, so liquidity isn’t a problem. But 5.7 is still bigger than 5.

It’s not that they won’t pony up $750K to make their pro-rata portion of the capital call… it’s that they can’t.

Which means that the XYZ Ventures—remember, those guys who try to carry a balance of zero?—don’t have East Virginia’s money to invest. Surprise!

If you’re the entrepreneur, you have to hope there are enough investors in XYZ Ventures who don’t have strict limits like this to fund an adequate capital call. But, even private pension funds that don’t have statutory allocation caps are still going to have internal targets. And 5.7 is still bigger than 5.

And that situation is going to continue until (1) the bulk of the portfolio value improves, or (2) until the VCs mark down enough valuations and shut down enough deals to get their proportion of LP assets back in line. The first is completely driven by the public market; have you checked the S&P 500 lately?

The second… writing down valuations makes the VC look decisive in the face of crisis, but it’s really going to play hell with their chances of raising money for their next fund. (And, just like Congressmen are always thinking about the next election, VCs are always thinking about their next fund. Always.)

Shutting down troubled companies makes the VC look equally decisive, but it eliminates the future requirement to keep investing in subsequent rounds of those companies. It’s a chance to clear the decks. And, heck, there will always be other companies to invest in, right? Plenty of fish in the sea.

To those CEOs of venture-funded companies who aren’t yet cash-flow positive… just because you’re not paranoid doesn’t mean they’re not out to get you.

If a VC firm make a capital call and an LP defaults, my understanding is they lose their entire position. Is this correct?

So, what if a fund is half invested and they want to make a new investment. And some LPs can make the capital call, but others cannot. Isn’t it a disservice to the LPs that do have funds and want it invested for the VC firm to not make the investment? Especially if it is a follow-on investment to a portfolio company that desperately needs the funds?

Does the VC firm play nice so they can raise their next fund? And let a portfolio company fail? Or do they make the call knowing some LPs will default (which is great for the remaining LPs)?

It’s completely dependent on the organizing documents of the limited partnership, and those really DO vary from fund to fund. Even within the same family, our default terms were very different in ATV-I versus ATV-III.

It might be that the defaulting LP is just cut out of future financings. It might be that their previous investments get converted to a note, to be payable in the sweet bye-and-bye. Or it might be that their portion of the partnership just vaporizes, leaving proportionally more for the investors who continue to invest.

This is ugly stuff, and I suspect a lot of funds and a lot of investors are going to be surprised by what got written into those thousand-page LP agreements…

CalPERS down 41% since 2007: http://tr.im/e9j4

Have you heard of many LPs defaulting on capital calls in Atlanta?